ranking companies Crystal forecasts monetary financial savings to upward push to Rs 315 lakh crore, or 74 p.c of the GDP via 2027, from Rs 135 lakh crore or 57 p.c ultimate fiscal.

While financial institution fastened deposits stay probably the most most popular monetary software within the nation, their percentage has declined over time, with buyers transferring against capital marketplace tools.

Fixed source of revenue tools, as observed of their penchant for financial institution fastened deposits, accounted for 41% of the family financial savings pie as of March 2022. Within the funding panorama, the proportion of fairness has larger from 24% in fiscal 2017 to 31% in fiscal 2022 whilst the proportion of different merchandise as represented via AIFs has grown from 1% to five% prior to now 5 years.

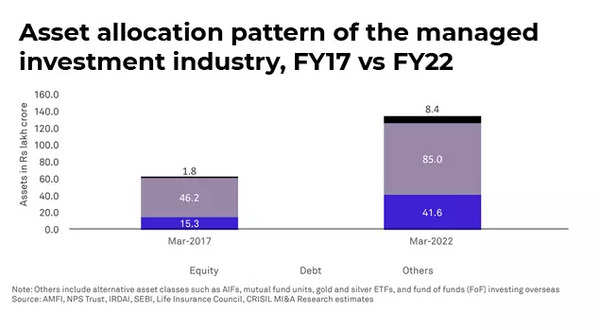

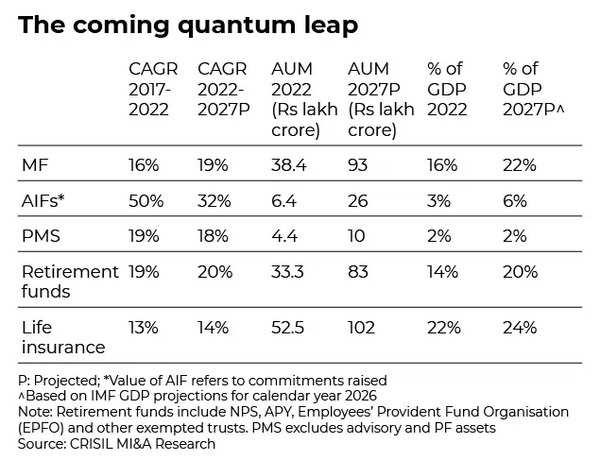

Assets of the controlled investments trade in India have greater than doubled in 5 years, from simply Rs 63 lakh crore in March 2017 to Rs 135 lakh crore in March 2022. By quantum, property of mutual budget and insurers leapt Rs 20 lakh crore every.

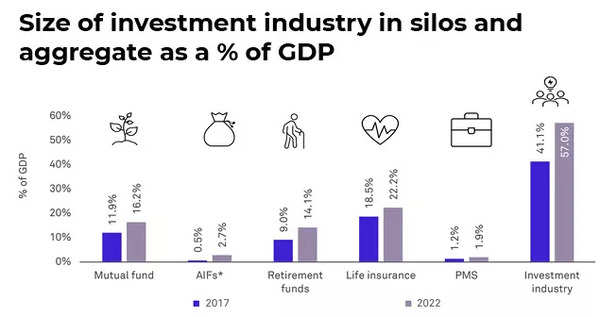

“As of last fiscal, AUM of the managed funds industry amounted to 57% of India’s gross domestic product,” stated Ashish Vora, President & Head, CRISIL Market Intelligence & Analytics. “In the following 5 years, we see this percentage emerging to 74% as financialisation will increase. Much has took place within the funding panorama over the last 5 fiscals, but the trade has slightly scratched the outside given the prospective in several classes and when compared with how such property have grown within the evolved nations.”

Household savings comprised over two-thirds of India’s gross savings except for the pandemic period when it shot up to 78% touching Rs 43.9 lakh crore.

Directed efforts at financial inclusion, digitalisation, a longer term trend of rising middle-class disposable incomes, and government incentives on these instruments, have better channeled these savings to the industry. With rising inflation, households too, are seeking higher returns beyond fixed deposits.

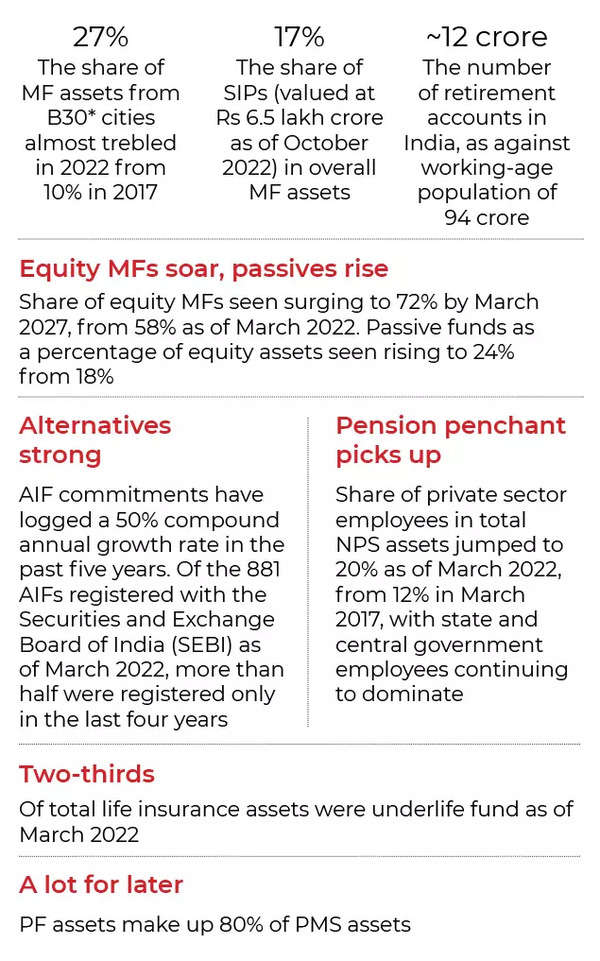

Life insurance companies comprised the biggest chunk of managed investments with a 39% market share at Rs 52 lakh crore. Mutual funds with assets under management of Rs 28 lakh crore and a market share of over 28% came next, the Crisil study showed. Though these still represent only 10% of households’ gross financial savings, they have gained from a big shift out of bank deposits.

CRISIL MI&A estimates the industry to grow to Rs 315 lakh crore in the next five years. And this growth will be led by a mix of macro and segment-specific factors.

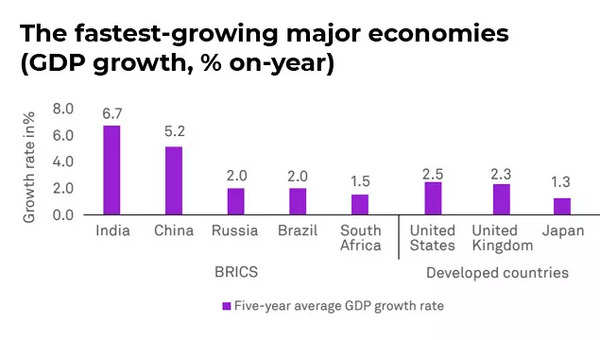

Strong GDP growth

CRISIL MI&A Research expects India to regain its tag of one of the fastest-growing economies globally in the medium term. The IMF has also forecast that the country’s GDP will grow at a faster pace compared with other economies.

Per-capita income surpasses inflection point

India’s per-capita income crossed the $2,000 threshold in 2021, ie, the inflection point when income crosses the subsistence expenditure level and moves on to spending and investments. India’s per-capita income expanded 7.6% last fiscal.

“High per-capita source of revenue, possibilities of robust financial enlargement, financialisation of family financial savings, emergence of generation, and get admission to to capital marketplace merchandise supply a fillip to the funding local weather within the nation,” said Crisil.

Rising middle-income population and demographic dividend

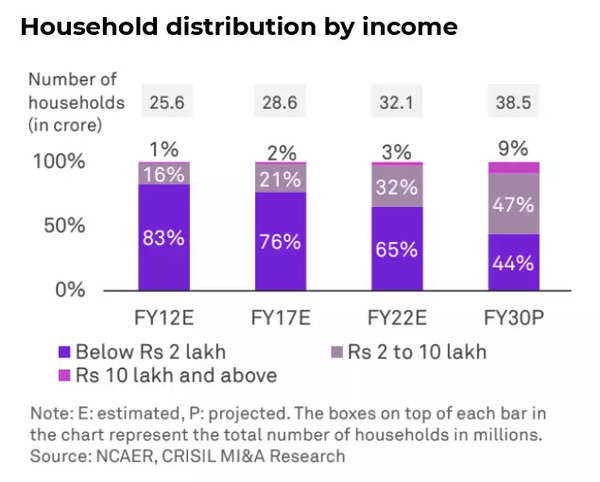

An estimated 83% of households in India had an annual income of less than Rs 2 lakh in fiscal 2012. That number reduced to 76% in fiscal 2017, and is expected to touch 65% this fiscal owing to the continuous increase in GDP and household earnings. The proportion of middle-income India — defined as households with annual income between Rs 2 lakh and Rs 10 lakh — has been rising over the past decade. CRISIL MI&A Research estimates there were 4.1 crore households in India in this category in fiscal 2012. By fiscal 2030, these are projected to reach 18.1 crore.That’s around 1.5 times the number of households (12.4 crore) in the US as of 2021.

As in step with United Nations inhabitants projections, about 94 crore other people, or 67% of India’s inhabitants, these days belong to the running age crew of 15- 64 years. This cohort will build up via 10 crore over the following decade, regardless of declining start charges.” Indeed, over the following decade, greater than a 5th (22.5%) of the incremental world body of workers will come from India,” said Crisil.

What is improving the financialisation of savings rate of Indian households?

India’s financial inclusion improved significantly over 2014-21 — the share of adult population with a bank account increased from 53% to 78% on the back of government measures and proliferation of supporting institutions.

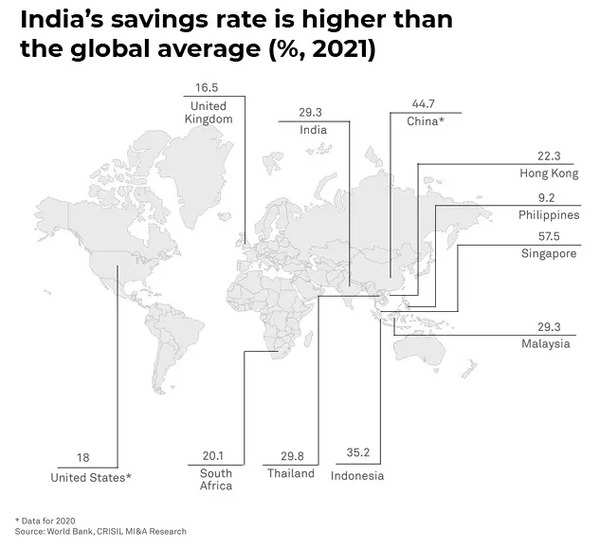

This is improving the financialisation of savings rate of Indian households, which is one of the highest in the world. At end-2021, the domestic savings rate of 29.3% was higher than the global average of 26.9%.

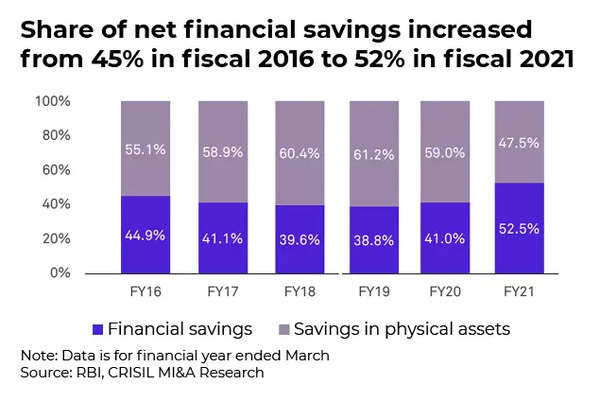

According to the RBI, the share of financial savings increased from 45% in fiscal 2016 to 52% in fiscal 2021, while that of physical savings fell from 55% to 48%.

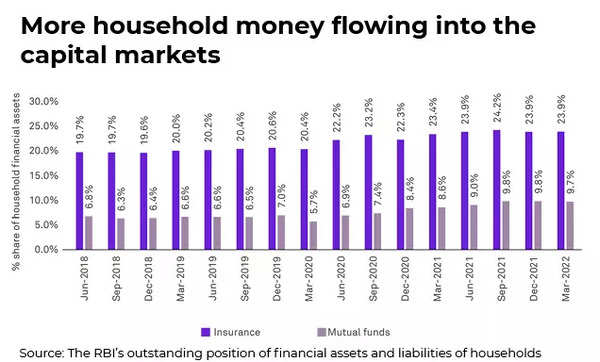

The money getting financialised is increasingly being invested in mutual funds and insurance funds. The share of mutual funds has increased from 7% in June 2018 to nearly 10% in March 2022, while the share of insurance funds has risen from 20% to 24% during the same period.

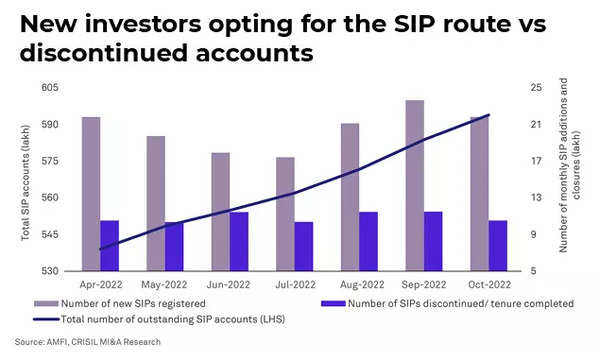

A living proof is the proliferation of SIP accounts to six crore as of October 2022, as much as 66 lakh accounts for the reason that get started of this fiscal.

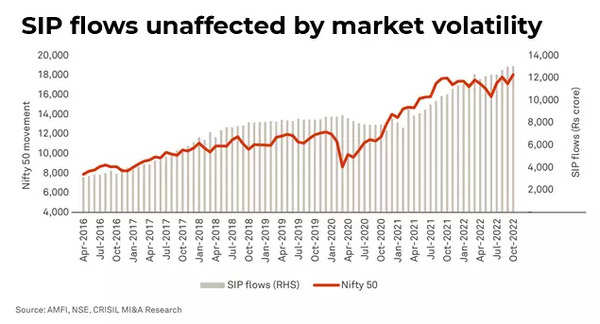

“The ratio of latest SIP accounts opened to these closed additionally stays wholesome, at about 2.4:1. Assets below SIPs crossed Rs 6.5 lakh crore as of October 2022, taking their percentage to just about 17% of the total trade AUM. Further, this Flow of cash into MFs has been rising regardless of marketplace volatility. SIP investments have larger from an insignificant Rs 3,000 crore as of April 2016 to over Rs 13,000 crore as of October 2022,” famous the learn about.

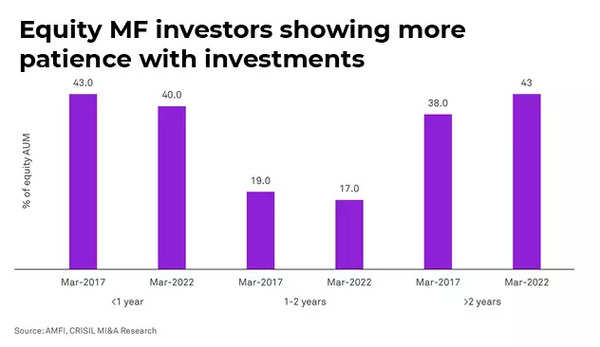

Even the adulthood horizon amongst buyers preserving budget for greater than two years has larger to 43% as of March 2022 from 38 p.c 5 years in the past.

Formal sector driving retirement funds growth

The formalization of the economy will be an important growth driver of the retirement fund industry as it brings individuals within the mainstream segment of the financial landscape. Subscribers from central government, state government and provident funds, which contribute mandatorily towards the retirement corpus, make up for 7.6 crore individuals. Voluntary contribution schemes such as NPS (corporate and unorganized sector), Atal Pension Yojana (APY), and Swavalamban have 4.4 crore individual subscribers.

The total number of accounts from these schemes is around 12 crore, compared with a working-age population of 94 crore individuals in the country.