At the height of the pandemic, charges had dropped to as little as 5.5% because of extra liquidity within the banking gadget and lots of had locked into 2-3-year deposits to make the most efficient in a depressed marketplace. Now with some personal banks providing 8% and public sector banks giving over 7.5%, savvy elders are having a look at untimely withdrawals to make recent deposits at upper charges.

A senior citizen in Mumbai had booked an FD of Rs 2.5 lakh in 2020-end for 3 years at 5.75% in a non-public financial institution with the assistance of her son. Upon finding out that the speed had risen to 7.75% for a similar tenure, the son not too long ago broke the FD and rebooked it. His mom gets an incremental source of revenue of just about Rs 20,000.

Last month, the federal government greater the returns at the senior citizen financial savings scheme (SCSS) with charges regaining the 8% stage after falling to 7.4% all through the pandemic. However, the distance between SCSS and financial institution FDs has diminished.

Some banks are providing even upper charges for “super senior citizens”, or the ones over 80 years. For example, Union Bank of India It gives 75 foundation issues (100bps=1 proportion level) over its common price for tremendous seniors, this means that they may be able to get 8% on 700-day deposits. Punjab National Bank gives tremendous senior voters 80bps over the common price and the best possible go back for them is 8.1% on 666-day deposits. Indian Bank gives this class of buyers 25bps greater than different senior voters.

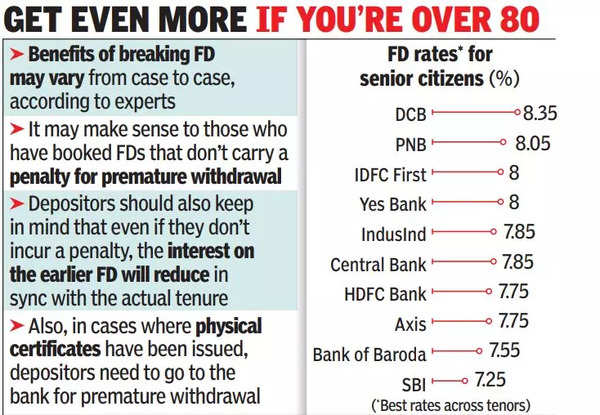

Another Mumbai-based retiree broke an FD that he had booked not up to a yr in the past to get a price that used to be just about two proportion issues upper. While those buyers mentioned they didn’t incur a penalty, mavens mentioned the advantages might range from case to case.

“Breaking an existing fixed deposit may be beneficial to some customers who have invested in FDs that don’t carry a penalty for premature withdrawal,” he mentioned. Gaurav Guptafounder & CEO of lending platform MoneyWide.

Even if there’s no penalty, the passion at the previous FD shall be diminished in sync with the true tenure, Gupta added. Another level to notice is that FDs may also be damaged on-line provided that they’re booked the use of netbanking. In instances the place bodily certificate had been issued, depositors want to pass to the financial institution for a untimely withdrawal. Experts mentioned that depositors will have to method a monetary marketing consultant to resolve if they may be able to take pleasure in a transfer.

Meanwhile, the RBI has greater the rate of interest on its floating price financial savings bonds to 7.35% from 7.15%. This has adopted the rise within the National Savings Certificate to 7%.

Some advisors additionally recommend liquid mutual finances as a substitute for deposits taking into consideration the indexation receive advantages this is to be had for investments over 3 years. However, those aren’t as secure as mounted deposits and their valuation can range along side the marketplace price of the underlying bonds.

Besides banks, non-banking finance corporations are providing sexy returns. HDFC’s “Sapphire” deposit scheme gives as much as 7.6% rate of interest. The loan large offers upper returns if the deposits are made on-line and if buyers are shareholders. For senior voters who’re shareholders and use netbanking, the go back is solely in need of 8%. Bajaj Finance Offers senior voters as much as 7.95% on three-year deposits.