While floating charges imply that debtors must pay the charges prevailing out there, this can be the most productive time to refinance loans as lenders are prepared to sacrifice a few of their margins for brand spanking new shoppers.

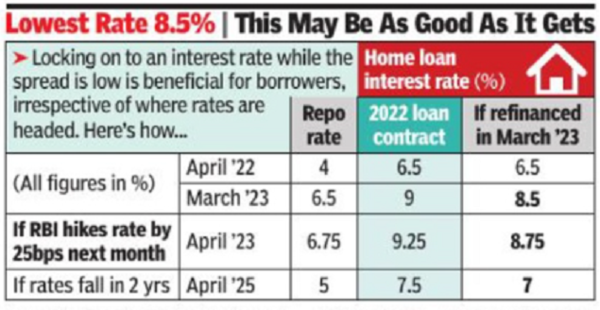

This supplies debtors a possibility to save lots of up to 100bps on loans. Bipin Salaskar, a central authority worker, had taken a Rs 59-lakh house mortgage at an rate of interest of seven.6% from HDFC a few years in the past. The charge in this mortgage has jumped to ten.1%, which has resulted in the mortgage tenure expanding by way of two years — past his retirement date.

“I approached other lenders to transfer my loan. I shifted to SBI as they offered me the loan at 75bps less,” Salaskar said. The revised EMI is lower and the original tenure has been restored, he added.

Most existing borrowers do not realize the impact of the increase in rates as they continue to pay the same equated monthly installments (EMIs). While their EMIs may not change, they will repay loans for many more years as rates climb up to make up for the higher cost.

If loan tenure gets extended when a borrower is close to retirement, due to rising interest rates, lenders usually seek an increase in EMI or a prepayment. Other lenders also offer to refinance loans at rates that are lower than what their existing customers are getting. Refinancing a loan typically entails a 0.5% processing fee.

Rohit Jaitpal, a private sector employee, got a home loan of Rs 50 lakh at 6.5% from HDFC last April, but the rate has now increased to 9%. As a result, Jaitpal’s loan tenure too went beyond his retirement age as it was extended by nearly three years. “I negotiated with HDFC and they offered me a lower rate of 8.5%,” Jaitpal stated. The lender does now not robotically decrease the speed to what it’s charging new debtors as it’s contractually sure to deal with the unfold over the repo charge during the time period of the mortgage.

Refinancing is smart for fresh debtors, even though the brand new charge is handiest 25bps decrease. Rate fluctuations hit debtors tougher within the preliminary years when the rate of interest part has the next percentage in EMIs. Hence, moving a mortgage is extra recommended for the ones with a number of years of EMIs forward of them.

Since 2019, all new house loans had been connected to an exterior benchmark charge just like the repo — the speed at which the RBI lends to banks. The RBI mandated the linkage basically to verify higher transmission of coverage charge adjustments. Lenders make a decision the unfold they’re going to deal with over a benchmark charge, in accordance with their price of finances and operations. They regularly stay the unfold low, particularly for brand spanking new shoppers to develop their trade.

During the pandemic, the RBI diminished the repo charge to 4% to spice up credit score expansion and spur the economic system. the least house mortgage charges then had been at 6.5%, which signifies a variety of 250bps over the repo charge. Currently, the repo charge is at 6.5% and a few banks are providing house loans at 8.5% to new shoppers, this means that the unfold has narrowed to 200bps.

According to business avid gamers, banks wouldn’t have a lot scope to supply higher offers. Currently, SBI’s best possible FD charge is 7.6%, whilst its most cost-effective house mortgage charge is 8.5% the unfold is simply 90bps. An opening any not up to this shall be unviable for banks.