While optimists are having a bet on central banks pivoting to rate of interest cuts, along side China totally rising from its Covid isolation and war in Europe abating, others are in search of dangers that can throw markets again into turmoil.

Below are 5 eventualities that threaten to carry extra hassle for buyers within the yr forward.

entrenched inflation

“The bond market is expecting inflation will pretty neatly come back into zone in 12 months,” mentioned Matthew McLennan, co-head of the worldwide price staff at First Eagle Investment Management.

But which may be a large mistake. There is an actual chance that wages expansion and supply-side pressures like increased power prices stay fueling shopper value positive aspects, he mentioned.

This would rule out the pivot to cuts from the Federal Reserve and European Central Bank that markets see coming in the midst of the yr.

The flow-on have an effect on: shares and bonds falling additional, greenback energy and extra ache in rising markets.

Then there is the query of upper borrowing prices triggering a recession and the way that performs out for buyers, in step with McLennan.

“The Fed didn’t see inflation coming and in their quest to fight inflation may not see a financial accident coming,” he mentioned. “It’s quite possible the Fed is underestimating the risk of financial catastrophe.”

China stumbles

Chinese shares have jumped about 35% from their October nadir at the prospect of the arena’s second-largest financial system totally reopening from long and draconian lockdowns.

Weighing in contrast optimism is the risk of the well being gadget being crushed as infections surge, and financial job collapsing. Crowded hospitals and queues at funeral parlors have led to alarm in contemporary weeks, and been accompanied through a drop off in social mobility in primary towns.

“China’s infection curve will rise and will only peak one or two months after Chinese New Year,” mentioned Marcella Chow, international marketplace strategist for JPMorgan Chase.

She expects the country to reach reopening however nonetheless cautions of “risk in terms of how Covid evolves.”

The rebound in Chinese equities stays fragile and any prospect of stumbling in financial job would sap call for in commodity markets, specifically for commercial metals and iron ore.

Russia-Ukraine conflict

“If the war worsened and if NATO became more directly involved in hostilities and sanctions ratcheted up, it would be quite negative,” mentioned John Vail, leader international marketplace strategist for Nikko Asset Management.

Secondary sanctions in opposition to Russian buying and selling companions, particularly India and China, would enlarge the impact of present restrictions at a deadly second for the worldwide financial system, in step with Vail.

“That would be a major supply shock for the world in terms of food, energy and other items like fertilizer, certain metals and chemicals,” he mentioned.

An much more alarming state of affairs could be the usage of a tactical nuclear weapon through a Russia — a risk that looks far-off however inside the nation-states of risk. That may finish Ukraine’s agricultural exports in a single fell swoop.

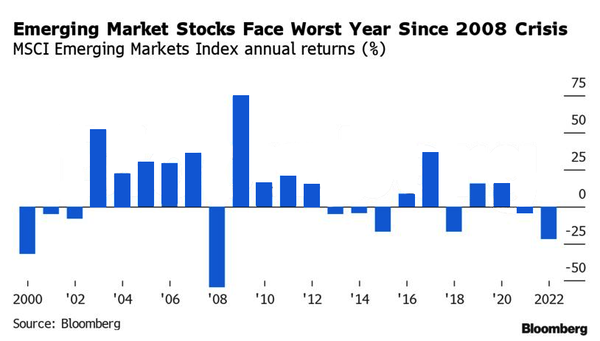

Emerging markets droop

Many buyers see greenback energy easing in 2023 and effort prices falling — two elements that may relieve power on rising markets.

Any failure to curb inflation would scuttle this result for foreign money markets, whilst an intensification of the conflict in Ukraine is solely one of the dangers that would ship power costs skyrocketing once more.

“We may well go through another year where emerging markets struggle,” mentioned Shane Oliver, head of funding technique and economics for AMP Services Ltd. “A still-high or possibly rising US dollar would work against emerging market countries because many have US dollar denominated debt.”

The ache from this state of affairs could be specifically acute for emerging-market governments that must endure an excellent heavier burden of debt raised in greenbacks.

covid rerun

A extra contagious or fatal pressure of Covid-19, and even the existing variants lingering longer, may start to jam up delivery chains yet again, which might ripple on into inflation and gradual financial job.

“We believe the macro hit to growth would be felt most by larger economies and those more dependent on trade,” mentioned JPMorgan’s Chow.

For now, she’s having a bet that the virus will proceed to recede and expects negativity in markets to be targeted extra on buyers pricing in recession in the USA and Europe.